Grow financial relationships with personalized experiences

learn more

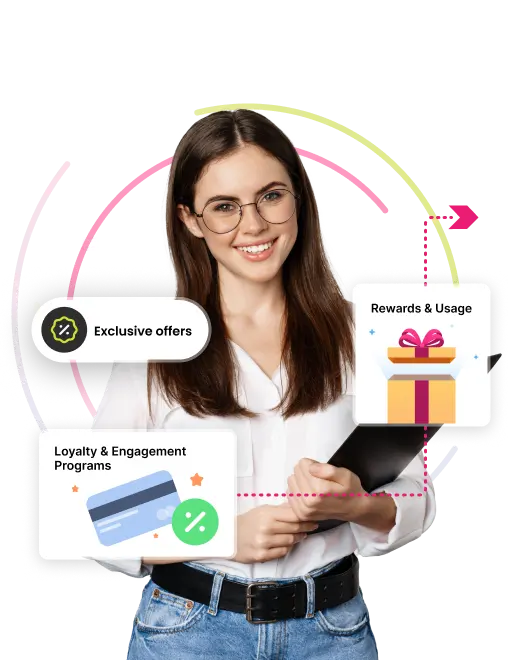

Power your financial institution’s experience layer

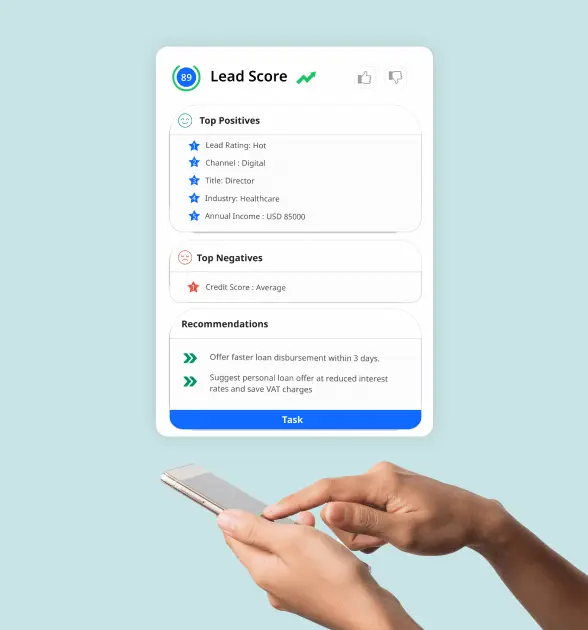

Take advantage of every interaction to advise in customers’ financial moments of truth. Power human and digital experiences with key insights and recommended actions.

Trusted Partnership with

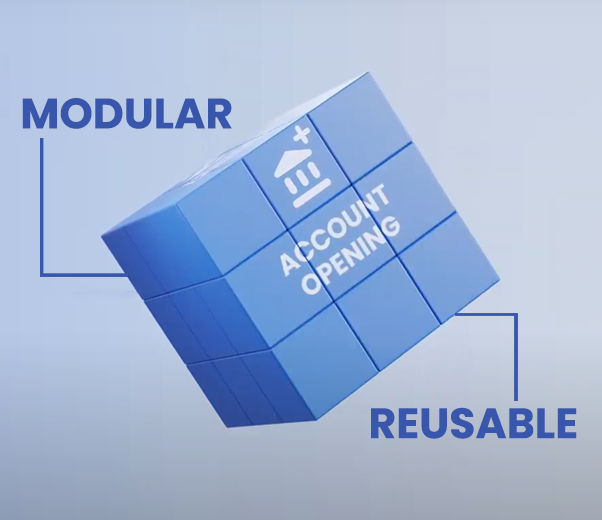

Packaged Solutions for Banks and Credit Unions

Deploy best-in-class and industry specific customer experiences to help your financial institution achieve its mission.

CRMNEXT Recognized as a leader

Gartner CRM Excellence Award for HDFC Bank Implementation

2023 Financial Service

CRM Wave

Celent Model Bank Award for HDFC Bank Implementation

2022 Best CRM Implementation for Axis Bank

Economic Times Award as the Best Organisation for Women

Insights & Trail Of Success

Boosting loans & deposits: The blueprint for credit unions to maximize CRM data strategy

Data is the key to unlocking a robust member experience. That’s because it enables CUs to learn deeply about members and predict and identify their next best needs. Doing this allows the credit union to demonstrate itself as a partner in their financial journey and conveniently position its products at just the right time. To succeed with data, credit unions need a strategy to bring data together and use it to drive actionable insights. A well-designed data strategy with a CRM can help credit unions unlock significant value.

learn More

Cultivating Leads, Loyalty, and Lifelong Customers with a Bank-Focused CRM

Combined with the right strategy and process, a CRM enables banks and credit unions to connect the dots throughout the entire customer lifecycle. With these insights, banks and credit unions can customize messaging, continually recommend the next best product for the individual, and foster long-term loyalty.

learn More

How to unlock the future: Predicting your members’ behaviors with CRM magic

For too long, credit unions have relied on the idea that knowledge + intuition would predict the future. But it doesn’t. All you get are vague assumptions, like some crystal-ball fortune-teller at a fly-by-night carnival. Sure, they’ll tell you what you want to hear. But you’ll lose money, time, and dignity in the process. To get real answers that retain (and attract) members, deepen relationships, and grow your credit union, you need to add data to the equation. Let’s take a look at these three magic words and how they, along with forward-thinking strategy and process, can make predictions possible for your credit union.

learn Morewhat our cutomers say

We all knew that deploying a next generation CRM tool was going to be a challenge, but necessary to continue our path as a digitally innovative credit union. CRMNEXT has helped us achieve that goal while demonstrating innovative approaches and a strong partnership. With the foundational pieces in place, we are building more modules to integrate disparate systems into a unified view that will benefit staff in all our member-facing as well as back-office teams.

CRMNEXT created a member-centric data model for OBEE Credit Union with a setup for integrating with several third-party systems. This unified view of our members has translated into efficiencies across our frontline teams. The outcome is simple: happy members and happy employees - a recipe for success and foundational to our culture.

We are living in an extraordinary financial environment. Banks and credit unions feel the squeeze with rising rates and margin compression. It is more important than ever to understand our members’ needs and respond to them swiftly. Adding more people is not the answer, nor is it getting any easier to recruit and retain staff. Communication and enabling our teams is critical, and this is a shortcoming of legacy systems. Now is the time to invest in CRM solutions and truly harness the power of information across the organization. We chose CRMNEXT to partner with us and to power our experiences.

CRMNEXT is our strategic partner to deliver digital transformation across our credit union. We leverage their technology to overhaul and unify member service processes into one single point of view. We have completely reimagined our service request and delivery process, referral management, and complaint workflows. We continue to innovate and engineer processes and procedures around the CRMNEXT platform to deliver great experiences to our staff so that they are engaged and deliver superior service to our members.

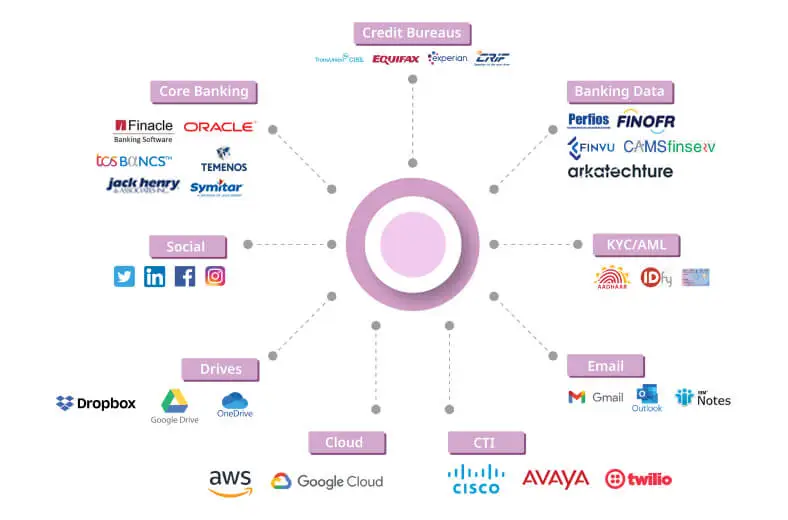

Ecosystem connectoR

UNLIMIT YOUR TRUE POTENTIAL. #UpForTomorrow!

You’re curious and caring, someone excited about solving the hard problems with technology. Fear of the unknown doesn’t hold you back from acquiring new skills to become truly ready for the future and #UpForTomorrow.